The current VLCC orderbook boasts 295 vessels, 151 of which were ordered since January 1st. In total, the orderbook now represents roughly one-third of the existing VLCC fleet. The ordering pace is already more than double the total contracted during the full year of 2025 and more than eight times the number ordered just three years ago - and it’s only July. They're doing so at roughly $131 million per vessel, among the highest newbuilding prices the industry has ever seen, while delivery slots stretch into 2030.

At first glance, this feels familiar. Strong freight markets. Robust balance sheets. Another ordering cycle. Oversupply. Freight rates drop. Haven’t we seen this movie before? Or is this time fundamentally different?

The conventional explanation is straightforward. VLCC earnings remain comfortably above $100,000 per day, Owners have generated extraordinary cash flow over the past several years, financing has become more accessible and confidence has returned. When markets are strong, Owners order ships. That's how shipping has always worked.

But that explanation only answers why Owners can order. It doesn't explain why they're willing to pay record prices for ships they won't see for another three years. That's a much bigger decision.

Every newbuilding contract signed today is effectively a forecast of the world in 2030 and beyond. It's a view on where oil will be produced, where it will be refined, how it will move across the globe and whether the political and economic forces reshaping tanker markets today will still exist tomorrow. In other words, Owners aren't simply forecasting freight rates. They're forecasting geopolitics.

Consider what they're trying to underwrite. The Strait of Hormuz, through which nearly one-fifth of global oil consumption passes, remains one of the world's most consequential geopolitical flashpoints. Russian sanctions continue to redraw global crude flows. The Red Sea has transformed from a routine transit into a strategic risk calculation. Every period of heightened tension forces charterers, traders and shipowners to reconsider routing, insurance, fleet deployment and contingency planning, even when the waterway itself remains open. Five years ago, these were considered extraordinary events. Today, they're increasingly embedded in the economics of moving oil. That's an important distinction.

For decades, shipping rewarded efficiency. The shortest voyage, the fastest turnaround and the most direct trade were the hallmarks of a healthy market. Today's market increasingly rewards resilience. Longer voyages, fragmented crude flows, sanctions, regional conflicts and shifting trade alliances have introduced inefficiencies that many Owners now appear to view not as temporary disruptions, but as structural characteristics of the market itself. If that's true, then the investment case for additional tonnage looks very different than it would through the lens of previous cycles.

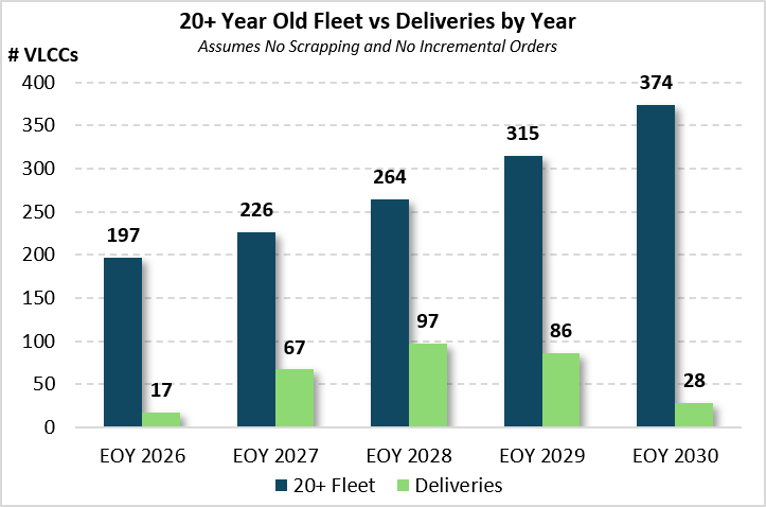

Then there's another statistic that's received far less attention than the orderbook itself. The global VLCC fleet stands at approximately 926 vessels and, on paper, adding another 295 ships sounds substantial. But headline fleet statistics can be deceiving. Approximately 205 VLCCs, representing more than 22% of the world's fleet, are now estimated to operate within sanctioned or shadow trades. The average age of the shadow fleet is roughly 23 years, compared to the age of the total global VLCC fleet: 13.5 years. The fleet itself is also aging with nearly half of all VLCCs are already 15 years or older, while almost 200 have surpassed the 20-year mark.

Commercially, many of these vessels no longer compete for the same business. For oil majors, national oil companies and many mainstream charterers, those vessels are effectively unavailable. They operate in a different commercial ecosystem, serving different counterparties under very different constraints. That's why the industry's focus on gross fleet growth may be missing the more important story.

Shipping doesn't trade on nominal supply. It trades on effective supply. The difference has rarely mattered more. Viewed through that lens, a 295-vessel orderbook looks less like an indiscriminate expansion of capacity and more like a response to a market where commercially available, and age appropriate, tonnage is tighter than headline numbers suggest.

None of this eliminates the risks. Shipping has a long and expensive history of extrapolating strong markets too far into the future. If geopolitical tensions ease, sanctions are lifted, trade routes normalize or oil demand disappoints just as this wave of new tonnage begins delivering, today's confidence could quickly become tomorrow's overcapacity. That's entirely possible. But perhaps the bigger mistake is assuming this cycle will behave like the last one.

Owners are committing billions of dollars at historically high asset prices, despite extraordinary geopolitical uncertainty and despite knowing those ships won't trade for several years. That's not speculation born of exuberance. It's a reflection of how they believe the world is evolving.

Perhaps the defining feature of this ordering cycle isn't optimism. It's conviction. Conviction that inefficiency has become embedded in global energy trade. Conviction that geopolitical friction is no longer an exception but an expectation. Conviction that effective tanker supply will remain tighter than conventional fleet statistics imply.

Time will decide whether that conviction proves right or wrong. But the next time someone points to 151 VLCC orders in just 7 months and asks whether the industry is overbuilding, perhaps there's a better question to ask first.

Are we counting correctly?